GST invoice is the primary commercial document that is issued by the supplier of goods or services to the recipient, and it is also issued to the seller of goods in some cases.

In general, it can be said that is a document around which GST sales, purchases, sales returns, and purchase returns revolve around. Proper and correct GST invoicing helps both the supplier and the recipient with correct accounting and payment of GST liabilities. GST invoice is the base document on which the GST return filing date is prepared for GST monthly return filing

Broadly speaking, the GST invoice identifies the supplier, and recipient, and provides information about the description of goods quantity of goods, date, mode of transport, and other price-related details. Apart from mandatory details required by SEC 31 of the CGST act for the practical purpose it is advisable to add details of payment terms, bank details, etc.

GST Invoice Vs Bill of Supply?

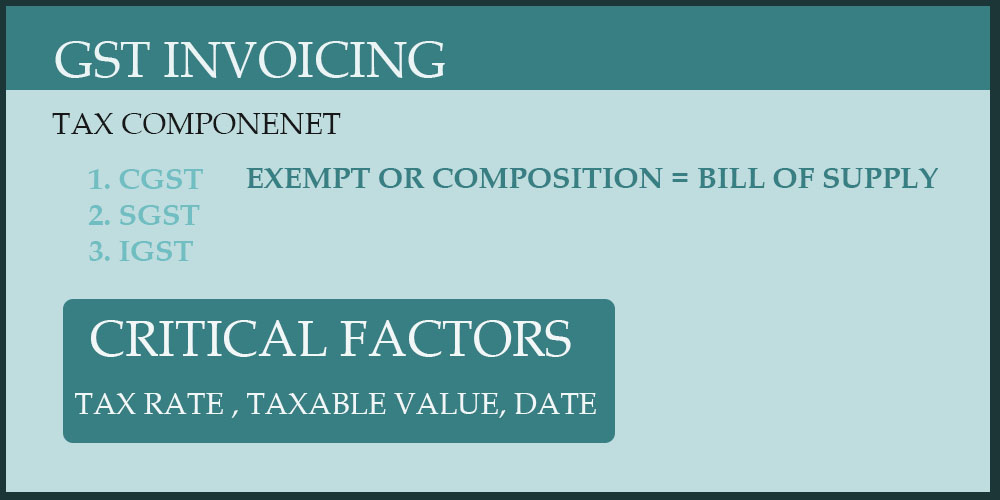

The GST-registered dealers will generally issue GST invoices to the recipient but in the case of the dealer registered under the composition scheme, a bill of supply will be issued by the supplier, similarly in the case of exempted goods or services bill of supply will be issued by the supplier.

A Bill of supply is similar to an Invoice without tax calculation having the words mentioned as a bill of supply.

Contents of Invoice or Invoice format

The proper invoice shall contain all the below details

- Serial number of the invoice, which is consecutively numbered

- Date of Invoice

- Name, Address, GSTN of supplier and recipient

- If the recipient is unregistered and the value of goods or services is more than Rs.50,000 then details of the HSN / SAC code shall be mentioned.

- Description, quantity, rate, and unit of goods or services shall be mentioned.

- The total value, taxable value, discount, tax amount, and tax rate are separately shown as IGST, SGST, CGST, etc.

- Address of delivery

- Details regarding reverse-charge

- Signature of the authorized person.

How do I mention the invoice date for the sale of goods or services?

In case the dealer is selling goods, the date of the invoice shall be before or at the time of removal of goods or when the goods are available for the recipient to take delivery or any time before that. In simple terms, the invoice date should be on or before the sale of goods, which was for the recipient to take delivery. To give a clear picture as GST return filing consultant, let me provide a simple real-life example below

Eg: Mr. Satish gets an order from Mr. Ravi on 27/05/2022 and a payment of Rs.1000 was made for the goods worth Rs.15,000 on the same day and the balance amount is payable on credit, Satish allows taking the delivery of goods on the 28/05/2022. In this case, even though the sale order is confirmed only on the 27th, but delivery is not provided on the same day date of the invoice shall be 28/05/2022 (the date on which goods are available for delivery).

Similarly, in the case of a supply of services, an invoice can be issued before the supply of services or after the supply of services, but when an invoice is issued after the supply of services it shall be issued within 30 days from the date of supply of services.

Eg : Mr. Satish gets the order from Mr. Ravi on 25/05/2022 and work is completed on 31/05/2022. In this case, the invoice can be issued any time on or after 25/05/2022 or within 30 days after 31/05/2022 (date of completion).

So the time limit is From 25/05/2022 to 30/06/2022, within this period invoice shall be issued to the recipient of services.

How to issue an invoice in case of advance payment by the recipient?

The invoice shall not be issued for each advance receipt, instead, the supplier needs to issue a receipt voucher for the amount received with all the details that are contained in the invoice in addition to the amount received. If the tax rate at the time of advance payment is not known, GST rules permit the use of the rate of 18% for tax calculation.

When to issue a credit note or debit note?

- A credit note is issued when the value of goods or tax amount charged is more than actually what it should be, and the credit note is issued to the recipient.

- In simple terms, where the invoice total is reduced, a credit note is issued.

- A credit note shall be consecutively numbered and filed in the month respective month.

- Credit note document shall clearly mention the words “CREDIT NOTE”.

- All the Information related to the supplier and recipient that will be added to the Invoice shall be present in the credit note.

- Clear details about the amount of credit against the taxable value and tax shall be presented.

- Similarly, the debit note is issued when the tax amount or taxable value needs to be increased from the original amount.